The Impact of COVID-19: Five Key Takeaways from NIC MAP’s 2Q20 Seniors Housing Data Release

July 31, 2020

NIC MAP® Data Service clients attended a webinar in mid-July on the key seniors housing and nursing care data trends during the second quarter of 2020. Led by the NIC research team, the webinar presented findings that reflected the impact of COVID-19 across the seniors housing and care sector. Key takeaways included the following:

Takeaway #1: Seniors Housing Occupancy Fell Sharply in 2Q 2020

- The all occupancy rate for seniors housing fell 2.8 percentage points in the second quarter to 84.9%, the lowest level since NIC has been reporting the data in 2005. This drop in occupancy was directly related to the COVID-19 pandemic as net demand fell by an unprecedented 15,100 units. Separately, new supply decelerated to its slowest pace since the first quarter of 2019.

- For perspective, its notable that the drop in net occupied units or absorption, while very large, only pushed total occupied units back to the level of the first quarter of 2019.

- Stabilized occupancy for all seniors living properties, defined by NIC as properties that have been open for at least two years or, if open for less than two years, have already reached a 95% occupancy level, fell by 2.9 percentage points to 86.9%, also a record low.

- The gap between all occupancy and stable occupancy was largely unchanged at 2.0 percentage points.

Takeaway #2: One of Five Properties Had 95% or Higher Occupancy

- There is a wide range of property level performance within the largest metropolitan markets. The average occupancy rate alone is not a tell-all indicator of a metro market.

- The median occupancy rate—which is defined as the mid-point of the distribution, with an equal number of properties below that rate as above that rate—is pulled higher compared with the average occupancy rate because 22% of the properties had a 95% occupancy rate or higher. Additionally, more than 43% of all properties had rates higher than 90%. This may be surprising to some.

- There was a large drop in the number of properties with an occupancy rate above 95%, however. This fell from a share of 33% in the first quarter to 22% in the second quarter.

- The average occupancy rate is being pulled down by the 28% of properties with occupancy rates below 80%, and the 40% of properties having occupancy rates less than 85%.

- Weaker occupancy rates were more prevalent in the second quarter. In the first quarter there were a lesser 31% of properties with occupancies below 85% (versus 40% in Q2) and only 22% with occupancies below 80% (versus 28% in Q2).

Takeaway #3: Largest Occupancy Declines Were in the April Reporting Period

- NIC MAP now offers Intra-Quarterly data results through June by metro area.

- Over the April, May, June three-month reporting periods, Denver had the largest drop in occupancy, falling nearly 5 percentage points from 87.9% to 83.2%, followed by St. Louis, Sacramento, and Orlando. The smallest decline in occupancy occurred in Cleveland, Washington, D.C., and Baltimore.

- In most instances the largest drops occurred in the April reporting period with lesser deteriorations in the May and June reporting periods.

- Two markets saw a bit of improvement in the June reporting period—Sacramento and Cleveland.

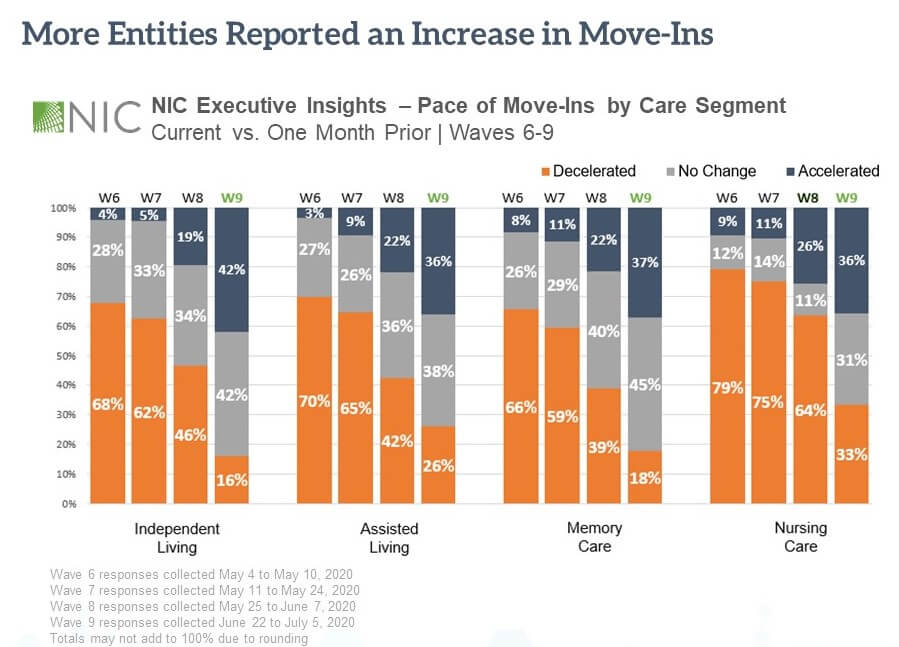

Takeaway #4: More Entities Reported an Increase in Move-Ins

- Since the onset of the pandemic, NIC has been conducting a regularly issued Executive Survey, a survey being conducted by NIC to get timely insights into the impact of COVID-19 on operators in the seniors housing and skilled nursing.

- In Wave 9 of the Executive Survey, the shares of organizations reporting an acceleration in move-ins in the past 30-days—across each of the care segments—is the highest in the time series (March 24 to July 5, 2020), while the shares of organizations reporting deceleration in move-ins is the lowest.

- As shown in the chart below, in Wave 9 of the survey, between 36% and 42% of organizations reporting on their independent living, assisted living, memory care, and nursing care segments noted that the pace of move-ins accelerated in the past 30-days. This is the second consecutive wave showing an increase of organizations reporting accelerated move-ins in the past 30-days, and the highest in the time-series, March 24 to July 5. The independent living care segment saw the most growth in the shares of organizations reporting an acceleration in move-ins between Wave 8 and Wave 9 (from 19% to 42%). Comparatively, between 16% to 26% of organizations with independent living, assisted living and/or memory care units, and 33% of organizations with nursing care beds reported that the pace of move-ins decelerated in the past 30-days—the smallest shares reported in the time series.

- Reasons cited by survey respondents for either an acceleration or deceleration in move-ins varied. In Wave 9 of the survey—as some state and local governments had lifted COVID-19 contagion spread mitigation measures, prompting some organizations to resume pre-pandemic planned move-ins, just over a third of respondents cited an organization-imposed ban or resident or family member concerns as reasons for slumping move-in rates--the fewest since the survey’s inception.

Operators are invited and encouraged to help provide transparency to the market by participating in the next Executive Survey. Click here to complete the survey.

Key Takeaway #5: All Buyer Activity Relatively Weak in 2Q 2020

- Based on this preliminary data, transactions volume in the second quarter totaled only $1.2 billion, which is not very surprising given the pandemic and the challenges within seniors housing and care that were present in the second quarter. That $1.2 billion represented a 64.3% decline from the first quarter of 2020 when volume registered $3.2 billion and a 70.4% decline from a year ago when volume registered $3.9 billion in the second quarter of 2019. For the year-to-date, transaction volume totaled $4.4 billion.

- Overall buyer activity was depressed with the topline dollar volume of only $1.2 billion, but one of the bright spots, although off a very small base, is the increase in activity from the institutional buyer in the second quarter.

- The institutional buyer activity increased 220% from the first quarter to register $309 million in closed transactions. Note however that this is coming off a very small base in the first quarter with only $97 million closed.

Interested in learning more?

While access to the full presentation of the key takeaways from this article is available exclusively to NIC MAP clients, the abridged version of the 2Q20 Data Release Webinar & Discussion – featuring data graphs and my commentary – is available through the link below.

Download Abridged Presentation

Now more than ever, the actionable data provided by NIC MAP® Data Service can help you stay informed. To learn more about NIC MAP and accessing the data featured in this article, schedule a meeting with a product expert today.

About Beth Mace

Beth Burnham Mace is the Chief Economist and Director of Outreach at the National Investment Center for Seniors Housing & Care (NIC). Prior to joining the staff at NIC, she served as a member of the NIC Board of Directors for 7 years and chaired NIC’s Research Committee. Ms. Mace was also a Director at AEW Capital Management and worked in the AEW Research Group for 17 years. While at AEW, Ms. Mace provided primary research support to the organization’s core and value-added investment strategies and provided research-related underwriting in acquisition activity and asset and portfolio management decisions. Prior to joining AEW in 1997, Ms. Mace spent ten years at Standard & Poor’s DRI/McGraw-Hill as the Director of the Regional Information Service with responsibility for developing forecasts of economic, demographic, and industry indicators for 314 major metropolitan areas in the U.S. Prior to working at DRI, she spent three years as a Regional Economist at the Crocker Bank in San Francisco. Ms. Mace has also worked at the National Commission on Air Quality, the Brookings Institution and Boston Edison. Ms. Mace is a member of the National Association of Business Economists (NABE), ULI’s Senior Housing Council, the Urban Land Institute and New England Women in Real Estate (NEWIRE/CREW). In 2014, she was appointed a fellow at the Homer Hoyt Institute and was awarded the title of a “Woman of Influence” in commercial real estate by Real Estate Forum Magazine and Globe Street. Ms. Mace is a graduate of Mount Holyoke College (B.A.) and the University of California (M.S.). She has also earned The Certified Business Economist™ (CBE), which is the certification in business economics and data analytics developed by NABE. The CBE documents a professional’s accomplishment, experience, abilities, and demonstrates mastery of the body of knowledge critical in the field of economics and data analytics.

NIC MAP Vision gives operators, lenders, investors, developers, and owners unparalleled market data for the seniors housing and care sector.