The Ongoing Impact of COVID-19: Six Takeaways from NIC MAP’s 3Q20 Seniors Housing Data Release Webinar

October 29, 2020

NIC MAP® Data Service clients attended a webinar in mid-October on key seniors housing data trends during the third quarter of 2020. Findings reflected the impact of COVID-19 across the seniors housing and care sector, led by NIC’s research team. Key takeaways included the following:

Takeaway #1: Seniors Housing Occupancy Fell Sharply Again in 3Q 2020

- The all occupancy rate for seniors housing fell 2.7 percentage points in the third quarter 2020 to 82.1%, the lowest level since NIC began reporting the data in 2005. This drop in occupancy was directly related to the COVID-19 pandemic as demand (as measured by net absorption) fell by more than 13,000 units. Combined with the second quarter, net absorption fell by more than 28,000 units.

- Separately, supply accelerated to 4,900 units, more than 1,000 units higher than in the second quarter.

- Since 1Q 2020 the occupancy rate has fallen an unprecedented 5.5 percentage points. The deterioration in the third quarter was just a bit less than in the second quarter.

- Stabilized occupancy for all seniors living properties, defined by NIC as properties that have been open for at least two years or, if open for less than two years, have already reached a 95% occupancy level, fell by 2.5 percentage points to 84.4%, also a record low. The gap between all occupancy and stable occupancy was 2.3 percentage points, reaching its record high difference seen in mid-2019.

Takeaway #2: Nursing Care Occupancy Fell Most in Past Two Quarters

- By property type, the pandemic took a toll its greatest toll on nursing care occupancy in the third quarter, with a drop of 4.2 percentage points from the second quarter to 76.0% in the third quarter. Combined with the second quarter drop of 6.5 percentage points, nursing care occupancy has fallen nearly 11 percentage points since the pandemic began. This reflects the fact that the COVID-19 virus has been particularly hard for frail elders and those with multiple chronic conditions and the fact that elective surgeries had been postponed during some of the months following the pandemic.

- Assisted living was next most affected with a 2.9 percentage point decline in occupancy to 79.1%. Combined with the 3.2 percentage point drop in the second quarter, there was a total loss in occupancy of 6.1 percentage points in assisted living since the beginning of the pandemic.

- Independent living saw a 2.4 percent point decline to 84.9% in the third quarter for a total two-quarter drop of 4.9 percentage points. This pushed the occupancy rate for independent living to a new low.

- In general, residents in independent living tend to be healthier than those in assisted living and nursing care, and hence the lesser decline.

Takeaway #3: Construction Starts Slowed Further in 3Q 2020 for Assisted Living and Independent Living

- Construction starts slowed in the third quarter, with 551 units of independent living initiated in the third quarter and 788 units of assisted living. On a four-quarter aggregate basis, independent living starts totaled 5,018 units, the fewest since 2013. As a share of inventory, this amounted to 1.5%. For perspective, at its peak in late 2017, it was 3.7%.

- Like other residential and commercial real estate sectors, starts are also being affected by tighter lending conditions and shortages in lumber and other key building materials.

Takeaway #4: Not-for-Profit Occupancy Decline Less than For-Profit

- The NIC MAP® Data Service collects data for majority assisted living and independent living property types, as well as community types such as CCRCs and stand-alone memory, and segment care types such as ADL-focused assisted living, memory care and independent living. They also track market fundamentals data by ownership structure such as for-profit and not-for-profit. These slices of data are all accessible through the NIC MAP Data Service on the NIC MAP Portal.

- Not-for-profit properties have consistently had higher occupancy rates than for-profit properties since the Data Service began reporting the data. The gap between the two ownership structures was smallest at 1.1 percentage points in the 2012/2013 period and has been widening ever since. Prior to the pandemic, the gap was a very wide 6.9 percentage points.

- In the third quarter, this gap grew to 8.8 percentage points, with the not-for-profits experiencing an average occupancy rate of 88.2% and the for-profits having an occupancy rate of 79.4%. The record wide discrepancy in the third quarter reflects the fact that occupancy for not-for-profits has held up better since the pandemic, with a 4.1 percentage point decline, while the for-profits saw a 6.0 percentage point decline to 79.4%.

- Part of the explanation is that not-for-profits typically have a larger share of independent living units which have been less impacted by the pandemic and a smaller share of assisted living units which have been more heavily impacted.

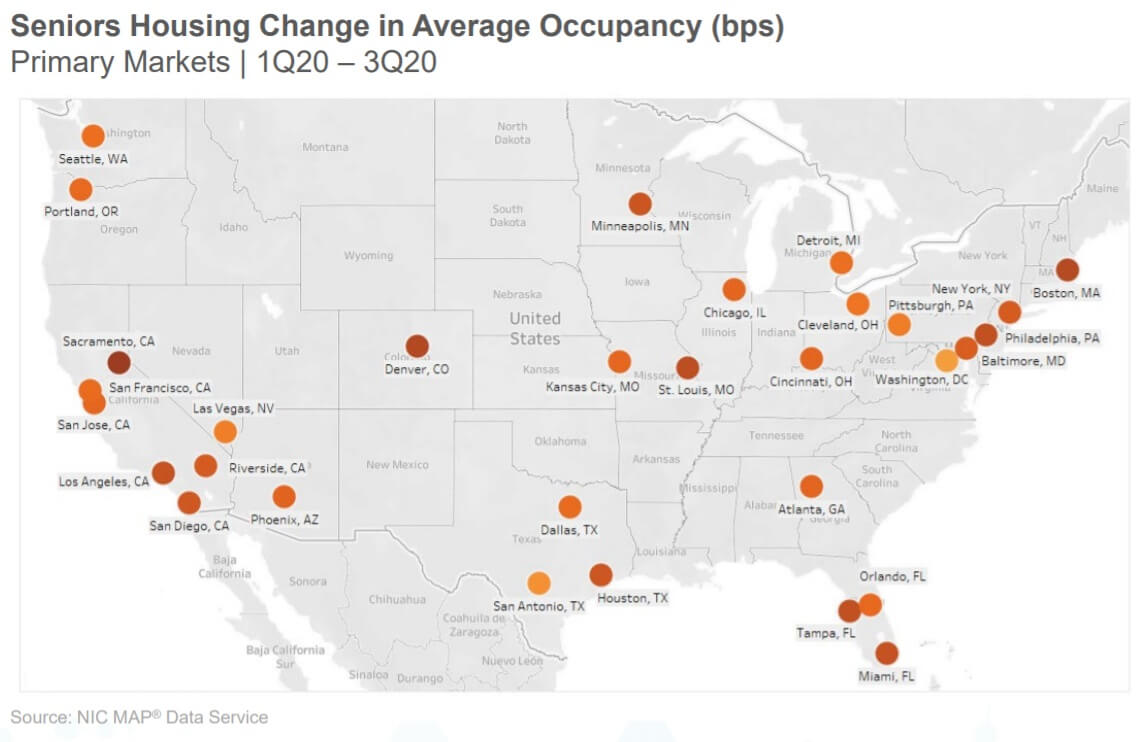

Takeaway #5: Seniors Housing Occupancy Declines Vary Across the Nation

- This map shows the degree of occupancy loss in seniors housing properties by metro area since the first quarter of 2020. The darker the color, the worse the occupancy rate decline. Since March, Sacramento, Denver, Boston, St. Louis have seen the most loss in occupancy, while Washington D.C., San Antonio, and Las Vegas experienced the least deterioration in occupancy.

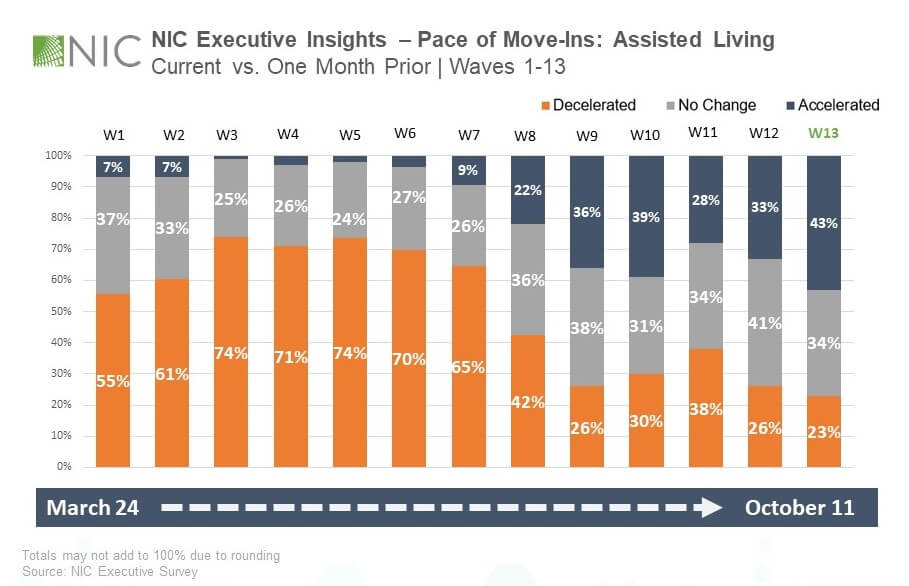

Takeaway #6: More Operators with Assisted Living Report Acceleration in Move-ins

- Since March, NIC has conducted a bi-weekly survey of owners and C-suite operators and executives of seniors housing and nursing care properties across the country in our Executive Survey Insights, The goal of the survey is to gather accurate, real-time information on current conditions and share these results with the industry. The data represents responses from small, medium, and large operators from both not-for-profit and for-profit providers. The data presented here shows findings from responses collected between March 24 through the week ending October 11th.

- Now currently in its 14th wave, this is the longest running survey of operators since the start of the pandemic, and NIC wishes to thank survey respondents for their valuable input and continuing support. The results of our joint efforts to provide timely and informative data to the market in this challenging time have been significant and noteworthy. These near-real time insights on the effects of the pandemic on senior living are being closely watched by the media and are working to help ensure the narrative on the sector is accurate.

- In this specific chart, the pace of move-ins for the assisted living care segment is examined across respondents’ portfolios of properties in the past 30 days. Focusing on the center of the chart—Waves 4 through 7, which included surveys from late April to late May, much of the country was experiencing widespread COVID-19 restrictions in physical distancing to mitigate the spread of the virus. Respondents reported organization-imposed and government-imposed moratoriums on admitting new residents, and thus difficulty backfilling residents lost due to normal attrition, residents moving to higher levels of care, and coronavirus illness and related move-outs—and the pace of move-ins ground down.

- By the end of July as shown in Wave 10, with move-in moratoriums easing across organizations, some residents waiting on sidelines with ADL needs could not wait to move any longer, and shares of organizations with increasing move-ins in assisted living was at the highest point to date. Recently, the shares of organizations with assisted living units that reported an acceleration in move-ins in the past 30 days increased in Wave 13 to the highest levels since the survey began in March.

Operators are invited and encouraged to help provide transparency to the market by participating in the next Executive Survey. Click here to complete the survey.

Interested in Learning More?

While the full presentation of the key takeaways from this article is only available to NIC MAP clients, you can access the abridged version of the 3Q20 Data Release Webinar & Discussion featuring my exclusive commentary below.

Download Abridged Presentation

Now more than ever, the actionable data provided by NIC MAP® Data Service can help you stay informed. To learn more about NIC MAP and accessing the data featured in this article, schedule a meeting with a product expert today.

About Beth Mace

Beth Burnham Mace is the Chief Economist and Director of Outreach at the National Investment Center for Seniors Housing & Care (NIC). Prior to joining the staff at NIC, she served as a member of the NIC Board of Directors for 7 years and chaired NIC’s Research Committee. Ms. Mace was also a Director at AEW Capital Management and worked in the AEW Research Group for 17 years. While at AEW, Ms. Mace provided primary research support to the organization’s core and value-added investment strategies and provided research-related underwriting in acquisition activity and asset and portfolio management decisions. Prior to joining AEW in 1997, Ms. Mace spent ten years at Standard & Poor’s DRI/McGraw-Hill as the Director of the Regional Information Service with responsibility for developing forecasts of economic, demographic, and industry indicators for 314 major metropolitan areas in the U.S. Prior to working at DRI, she spent three years as a Regional Economist at the Crocker Bank in San Francisco. Ms. Mace has also worked at the National Commission on Air Quality, the Brookings Institution and Boston Edison. Ms. Mace is a member of the National Association of Business Economists (NABE), ULI’s Senior Housing Council, the Urban Land Institute and New England Women in Real Estate (NEWIRE/CREW). In 2014, she was appointed a fellow at the Homer Hoyt Institute and was awarded the title of a “Woman of Influence” in commercial real estate by Real Estate Forum Magazine and Globe Street. Ms. Mace is a graduate of Mount Holyoke College (B.A.) and the University of California (M.S.). She has also earned The Certified Business Economist™ (CBE), which is the certification in business economics and data analytics developed by NABE. The CBE documents a professional’s accomplishment, experience, abilities, and demonstrates mastery of the body of knowledge critical in the field of economics and data analytics.

NIC MAP Vision gives operators, lenders, investors, developers, and owners unparalleled market data for the seniors housing and care sector.